Shame. It may be the single most corrosive force of our time.

When my husband and I were in our final year of the MFA program where we met, we were each responsible for producing a book-length thesis. Jason and I had started dating in our first year and moved in together quickly, realizing that spending every night together made paying two rents on graduate student stipends the fool’s way. We got lucky; by the time we began writing our theses, we were still together and had discovered that we were, despite the odds of ego, capable of being writers in the same one-bedroom apartment in Columbus, Ohio.

Where we differed, though, was in our habits. I think it surprised us to learn that my anxiety made me a diligent, if constantly worried, writer, while Jason’s narcotic calm led him to procrastinate. When I’d come from home from teaching during the final weeks of April leading up to our defenses, I’d find my normally levelheaded partner in a feral state: wild-eyed and pale, over-caffeinated and under-nourished. He’d temporarily taken up smoking, and it wasn’t uncommon for me to walk in on him digging an antler-handled knife into his pressboard desk, a rolled cigarette pursed between his lips, the whole scene trapped in smoke by the light of the bay window.

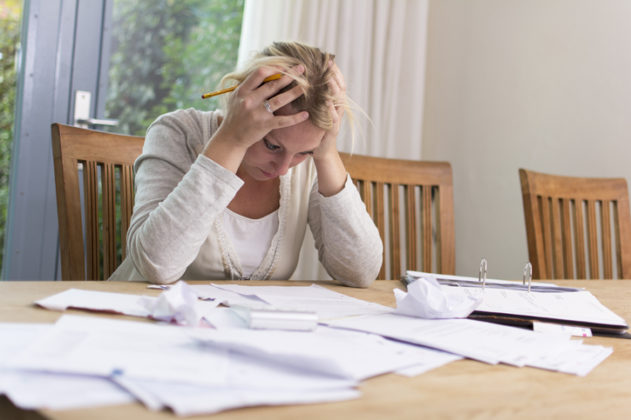

That image came to me last week when Jason did our taxes. Once again, we’d put it off all winter, so he asked me to entertain our 3-year-old daughter while he tackled the job in our room, promising it would only take an hour or two. When several more hours passed, and our daughter had exhausted her supply of movies and interest in painting, glitter glue, and costumes, I came to check on him. He was sitting on the bed, nested in a pile of W-2s and receipts. A cup of coffee sat beside him going cold on the nightstand, and his jaw tightened as he spoke by phone with the IRS.

I knew what it meant: We owed. Again.

Life never exactly stabilized for us after graduate school. We had terminal degrees and teaching experience in hand, but it was 2008, and the bottom had just dropped out of the U.S. economy. Tenure-track teaching jobs were already declining as the rise of adjunct labor made college professors come cheap, especially in the liberal arts. But now, with many colleges forced into hiring freezes, a single tenure-track position had several hundred applicants. This is still the case today.

To make matters worse, graduating from my MFA program meant that my undergraduate student loan deferment was up, and I immediately had a new monthly bill of $300 to pay. Add that to an outstanding medical bill for the early cervical cancer I had treated as a grad student, and combine that balance with the cost of moving from Ohio to Alabama for our first teaching jobs. We had to put the U-HAUL on Jason’s credit card, and take on a car loan so we could both commute to work.

We didn’t know it at the time, but by then, we were in deep enough debt that it’s now unlikely we’ll ever fully recover.

We moved for work two more times over the next five years (more U-HAULs, more rental costs). In 2012, my dad died, and though we did get a small settlement from his estate, the entirety of it went to paying costs that came when our daughter was born the following year. Because I had not been at my job long enough, I didn’t qualify for FMLA, and had to choose between returning to teaching after using my three weeks of sick leave, or taking the entire semester off unpaid. Having that choice makes me exceedingly lucky compared to most lower- or middle-income mothers. But we had to use all of the estate money to keep our bills paid during my maternity leave.

Yet another move followed when our daughter was six months old, our third move in six years. This time, we moved east to Boston for a tenure-track job that offered my family the chance of greater security and stable health insurance, and while I’m absurdly happy with my university, my colleagues, and my new city, there’s no getting around the dramatic cost of living increase. Boston is the third most expensive city in the U.S. for renters, and now we had childcare needs on top of rent.

Still, our financial problems are enviable, plus we have employer-based health insurance that keeps our minds and bodies in working condition. Today, Jason and I both have full-time jobs in our chosen field. We find meaning in what we do all day, and cheerfully have hours-long conversations about our classes, students, and writing. We don’t take vacations or have savings that last beyond the end of the month, but we occasionally splurge on delivery food, and will put off a bill for a week if we want to take our daughter to the zoo or aquarium. No one in our family has ever gone hungry or homeless.

But when our car broke down, we had no immediate funds to get it fixed. We had to leave it parked on the street, where its rear license plate was stolen, which led to a ticket from the city. During the intervening weeks before my in-laws generously came to our financial rescue, Jason and I took the train as often as we could, but sometimes had to spring for a Lyft. We also had to rent a car so that I could get to the conference in Washington, D.C., where I was scheduled to give a presentation, adding to the expense of professional development. And earlier this year, doctors discovered a tumor on my thyroid. When our insurance company wouldn’t pay for the recommended genetic test administered to avoid unnecessary surgery, we added it to the (comparatively small) pile of medical bills on my desk.

These are manageable money problems. We have friends whose debt far exceeds our own for all the same reasons we have, and many more we’ve been lucky not to. But there’s no getting around the shame we feel when we get to the end of another fiscal year and find our bank account in worse shape despite the effort and exhaustion of our jobs and parenting.

The subject of money is finally losing its cultural taboo. Maybe because the recession that began in 2008 has set an entire generation of Americans back from their goals of gainful employment, home ownership, and starting families, we can no longer take a polite attitude about the private hoops we jump through to pay our bills. This semester, I’m teaching a class in literary publishing, and one of the first articles we read was an in-depth New Yorker piece about Amazon’s stranglehold on the industry, which squeezes out profits for publishers and their authors alike. My students complained about the economic focus of the article—they were there to learn how to get their writing in print. But the two are linked, I explained. They would have to think carefully about how to finance their writing because writing itself won’t pay enough.

At the conference I attended in D.C., I noticed a burgeoning number of panels devoted to the economics of writing and publishing alongside the ones about how to land a tenure-track teaching position, or eschew academia altogether in favor of higher-paying day jobs. I’m grateful that books like Scratch: Writers, Money, and the Art of Making of a Living are finding their way into the conversation about how artists and academics have secretly been scraping by for years under the cover of advanced degrees and fancy job titles. Cheryl Strayed, a contributor in Scratch, said in a recent interview that she was $85,000 in debt when her bestselling memoir Wild was published. “We almost lost our house before I sold Wild,” Strayed says. “I can say that now because I don’t have any debt, but I was so ashamed of that.”

Shame. It may be the single most corrosive force of our time. After the election, we saw a spate of articles about the “hidden Trump voter,” too ashamed to admit their candidate. And now that we’ve got social media, we can shame one another with exacting, indelible skill. Screenshots are forever, they say, adding to our fears of presenting anything other than perfect Paleo meals, Instagram-filtered marriages, gifted children, and happiness, happiness, happiness, ever increasing happiness.

And in America, ever-increasing happiness translates to ever-increasing consumerism. The recession has popularized minimalism—KonMari, capsule wardrobes, tiny houses that have all become playthings of the rich—but the truth is that most of us already have too little, so cling desperately to the myths of upward mobility and bootstrapping, believing that America was, still is, the place where hardworking people get what they need. It has never been true, especially for minorities, but such hope temporarily neutralizes our shame.

Until the next bill. Until the next medical emergency. Until the next tax season. No wonder so many of us feel that ours is now a regressive country. Two-thirds of us are wild-eyed, pale, undernourished, over-caffeinated, and over-medicated, trying to insulate ourselves with whatever cheap comforts we can: booze, pills, cigarettes, food. And of course, we shame each other for that, too. Choose happiness, we say. Choose gratitude.

A few weeks ago, with our car fixed, we ventured to Cortland, New York, so I could give a reading at the state university there. I read the first chapter from my memoir-in-progress, and the audience heard me talk about the emotional ins and outs of grief and pregnancy. During the Q&A, a student asked me if there is anything I don’t write about, anything I deem off-limits in my work. “Money,” I told him, and went on to explain. I felt my face get hot, burning with embarrassment. Here I was, the guest speaker, a college professor, admitting to a room practically pulsing with the aspirations of undergraduates that my version of success doesn’t include home ownership or world travel.

But later, at dinner, a faculty member in the English department thanked me for my answer to that question. “I really appreciated hearing that,” she said. “I’m in the same boat.”

Amy Monticello is an assistant professor at Suffolk University. Her work has appeared in many literary journals, and at Salon, The Rumpus, and The Nervous Breakdown. She currently lives in Boston with her husband and daughter. Follow her on Facebook, Twitter, and Instagram.

Other Links: